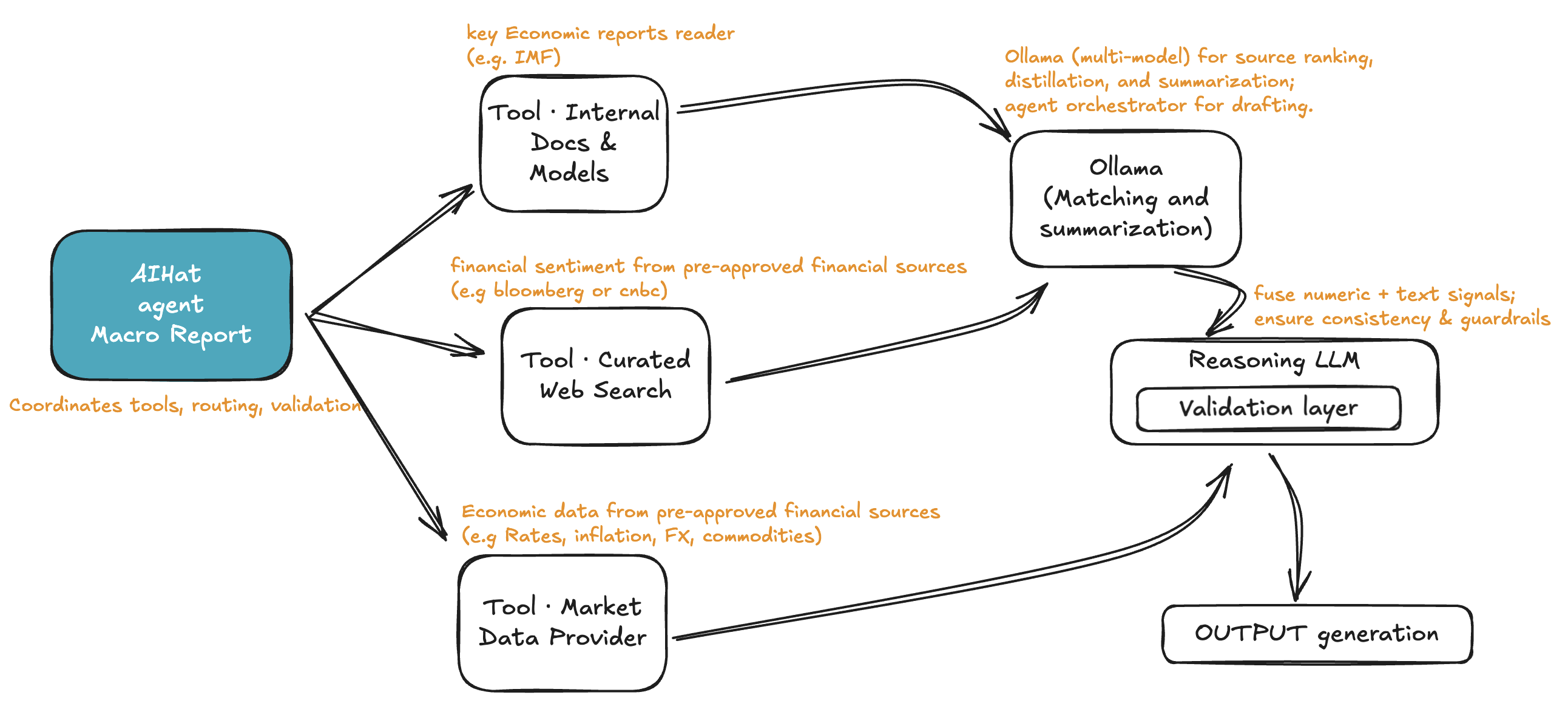

Executive Takeaway

Inflation has mostly normalised and central banks have stopped tightening, but real rates remain positive in key economies and equities have already rallied hard. Growth is slowing rather than collapsing, and the near future looks like a grind of modest policy easing and selective opportunities, not a broad new boom.

Stay patient, focus on quality, and be picky about where you add risk.

Decision Tile — From View to Action

Macro Pulse — Key Metrics

| Indicator | Latest | 1M Trend | Comment |

|---|---|---|---|

| US policy rate | 3.75% | ↓ | Cycle has turned to cuts; further gradual easing likely. |

| Europe main policy rate | 2.15% | → | Central bank can hold or trim cautiously, not aggressively ease. |

| Japan policy rate | 0.75% | → | Still low; keeps real rates negative and supports domestic demand. |

| Crude oil | USD 56.7/bbl | ↓ | Well below past spikes; eases headline inflation and input costs. |

| Natural gas | USD 3.9/unit | ↓ | Lower energy burden supports consumers and energy-intensive industry. |

| Gold | USD 4,552.7/oz | ↑ | Extremely elevated; reflects hedging against policy, inflation and geopolitical risks. |

| EUR/USD | 1.18 | ↑ | Above parity; creates FX headwinds for euro-based investors in US assets. |

Scenario Map — 6-Month Outlook

| Scenario | Probability | Policy Bias | Asset Implication |

|---|---|---|---|

| Gradual Disinflation Grind | base case | cuts; slow, data-dependent | Favor quality cyclicals, steepeners, selectively add EM and eurozone risk. |

| Sticky Inflation Pockets | ~30% | hold; cuts delayed, rhetoric hawkish | Trim duration, prefer value and financials, keep some commodity exposure. |

| Growth Scare / Risk-Off | ~20% | mild easing; faster cuts if data crack | Add high-grade duration, USD, reduce high-beta EM and cyclicals. |

Macro Landscape

The big picture is a world where inflation has largely cooled and central banks have stopped tightening, but growth is uneven and markets are already leaning into a better future. Policy is no longer getting tighter, yet the cost of money is still high enough to matter for credit and valuations.

On rates, the global centre of gravity has clearly shifted from hikes to cuts. The United States has lowered its policy rate to 3.75%. Europe holds its main rate at 2.15%. Japan has moved to 0.75%. Canada is at 2.25%. Switzerland is already at zero. The common thread is that the phase of ever-rising borrowing costs is over, so companies and households are no longer facing a steadily worsening interest burden.

Real rates show where policy is genuinely tight versus merely less loose. Japan runs a policy rate of 0.75% with inflation near 2.91%. That keeps Japanese real rates clearly negative. Switzerland has a zero policy rate and inflation near 0.02%. That leaves its real rate roughly flat. China’s policy rate near 3% with inflation under 1% produces a positive real rate above 2%. Türkiye’s very high policy rate and inflation near 31.07% still leave it with a clearly positive real rate. Positive real rates restrain borrowing and favour cash and short bonds over speculative growth stories.

Inflation has cooled almost everywhere, but the level matters. Canada, Germany and Italy now sit near or just above 2%. The United Kingdom is still closer to 3.57%. Japan is near 2.91%. Switzerland is almost at zero. China runs inflation under 1%. Türkiye remains an outlier above 30%. For investors, that means most advanced economies are back in a zone where central banks can think about modest easing, while high-inflation countries must stay restrictive.

Commodities tell you how tight real-economy conditions feel. Crude oil is around USD 56.7 per barrel. That is a far cry from previous energy spikes and eases pressure on headline inflation and on energy-intensive industries. Natural gas is around USD 3.9 per unit, which also points to easier input costs relative to the last energy shock. Gold trades near USD 4,552.7 per ounce. That is extremely elevated and reflects continued demand for hedges against policy error, inflation uncertainty, and geopolitical stress, even as inflation has fallen.

Currencies underline where the pressure points lie. EUR/USD trades around 1.18. That keeps the euro above parity, so for euro-based investors, US assets face a translation headwind if the dollar weakens further from here. When the euro strengthens, imports from the United States cheapen in euro terms, but US-dollar profits from global companies translate lower. The US dollar still acts as the dominant safe-haven currency, so sharp risk-off moves would likely still mean a stronger dollar and weaker cyclical and emerging currencies.

Labour markets show where growth is cooling versus cracking. US unemployment has risen to 4.4%. It was 4.1% one year earlier. That is an easing, not a collapse. Germany sits near 3.2%, slightly lower than last year. Japan holds around 2.5% with little change. Italy is around 7.2% and has edged up. Türkiye is near 9.9% and has also ticked higher. This pattern describes a global economy that is slowing at the margin but not in outright recession.

GDP levels confirm that growth is positive but not booming in most major economies. US nominal GDP is around USD 30.3 trillion. China’s is around USD 19.5 trillion. Germany’s is around USD 4.9 trillion. Japan’s is around USD 4.4 trillion. Italy’s is around USD 2.5 trillion. Türkiye’s is around USD 1.5 trillion. All these economies show nominal GDP above last year, helped by residual inflation and real growth.

Equities have already moved to price this environment. A broad developed-market proxy trades near 690.3. Over the past year, it has gained about 17.36%. An emerging-market proxy trades near 54.8. Its one-year gain is about 30.6%. A eurozone equity proxy trades near 64.33. Its one-year gain is about 36.47%. So emerging markets and eurozone equities have outperformed the US-led developed basket over the past year, helped by the pivot away from aggressive tightening and by lower starting valuations.

Putting it together, we are in a world where the tightening shock is behind us, inflation has mostly normalised, but real rates are still positive in key economies and equity markets have already front-run a friendlier growth-inflation mix. That is the setup for the forward view.

Forward View

The starting point for the outlook is that policy is no longer marching higher, but central banks remain wary. In the United States, the policy rate is already lower than its peak, and higher unemployment and contained inflation open the door to further, gradual cuts rather than fresh hikes. Europe’s 2.15% policy rate, plus inflation near 2% in Germany and around 1–2% in Italy, points to a central bank that can stay on hold or trim cautiously, but not swing to aggressive easing.

Japan stands out with a still-low 0.75% policy rate and inflation near 2.91%. That combination keeps Japanese real rates negative and supports domestic demand and equities, but also keeps pressure on the yen. China’s roughly 3% policy rate with very low inflation near 0.72% means real rates are firmly positive. That helps anchor the currency and contain leverage, but it also restrains private-sector risk-taking, especially in credit-sensitive sectors.

Positive real rates in China and Türkiye and flat-to-slightly-positive real rates in Europe and Canada point to a world where central banks are cautious about over-stimulating after the inflation shock. That means credit conditions will ease only slowly. For corporates, the cost of capital will likely fall from peak levels but remain well above the pre-pandemic era, which weighs on weaker balance sheets and favours companies with strong free cash flow.

On growth, rising US unemployment and slower business surveys indicate that US growth is likely to cool from recent strength but remain positive. Euro-area unemployment is stable or falling slightly in Germany, which fits with modest growth rather than contraction. Japan’s stable unemployment and ongoing nominal GDP gains fit with steady, if unspectacular, expansion. Italy and Türkiye have higher and rising unemployment, which warns that growth there is more fragile as tighter policy feeds through.

The FX and commodities setup frames relative winners. An above-parity euro with relatively low European inflation makes imported energy cheaper for Europe compared with recent years, supporting margins for energy-intensive industries. A still-strong dollar in global stress events would continue to tighten conditions for dollar borrowers in emerging markets, even as their equities have outperformed recently. Lower oil and gas prices help consumer economies but sap nominal growth in energy exporters.

Equities already reflect much of the good news. Developed-market stocks are up mid-teens over the year. Emerging-market and eurozone equities have gained far more. If policy easing continues but remains measured, leadership is likely to stay with markets levered to lower real rates and cyclical recovery, including parts of emerging markets and Europe. However, with gold at very elevated levels, markets also reveal ongoing hedging against political and policy shocks, which can cap valuation expansion if growth disappoints.

Relative to the latest multilateral outlook, which sees global growth near the low 3s and inflation trending lower, this base case is broadly aligned. Both views feature moderate growth, fading inflation, and lingering concern about public debt and fiscal space, rather than a deep downturn.

Overall, the forward stance is one of moderate growth, slow policy easing, and markets that are already pricing a fair amount of good news.

Short-term Market Themes (from recent headlines): policy easing chatter and geopolitics headlines dominate, with investors weighing slower data against ongoing earnings resilience.

Investment Relevance

- Tilt toward quality within equities as financing stays more expensive.

- Prefer positive-cash-flow cyclicals over long-duration growth at these real rates.

- Use gold and high-grade bonds selectively, not as all-weather hedges.

- Differentiate within emerging markets by inflation and external-funding needs.

- Hedge US exposure carefully if you are euro-based above parity.

- Stagger entry points; avoid chasing recent outperformance in eurozone and EM.

Edge Box

Markets are already pricing a smooth shift from tight policy to softer inflation and moderate growth, but still-positive real rates, especially in China and Türkiye, point to a slower easing in credit conditions and a tougher backdrop for weak balance sheets than price action suggests.

A clear growth stumble in major economies or a sharp euro reversal against the dollar would challenge the view that moderate expansion and orderly policy easing can coexist with elevated equity valuations.

Investors should stay selective, favouring quality and cash-generative names over broad beta, while treating gold strength as a sign of lingering tail-risk hedging rather than a green light for aggressive risk-on positioning.

Where We Might Be Wrong

- Underestimate inflation flare-up from energy or renewed supply shocks.

- Overestimate resilience of earnings as real rates stay restrictive.

- Misjudge policy reaction speed if unemployment jumps sharply.

Beginner’s Guide

Big Picture

Money is no longer getting tighter, but it still is not cheap, and stock markets have already cheered this. Growth in the world is slowing a bit, yet most places are not in deep trouble. For a small investor, this means the easy gains from the big policy shift may be behind us, so careful choices matter more than bold bets.

What It Means for You

Think in years, not weeks. Expect bumps, not a smooth climb. Focus on solid, boring holdings that can live with higher borrowing costs, instead of chasing exciting stories that need perfect conditions.

- Trim positions that ran up fast if they now feel too big or risky

- Add slowly to strong, profitable companies or broad funds instead of single hot ideas

- Spread money across regions so you are not tied to one country’s path

- Use any new savings to nudge your mix back toward your long-term plan

Looking Ahead

In the coming months, put most of your energy into your own habits, not the news flow. Set a simple check-in schedule so you review your portfolio calmly instead of reacting to every headline. Track how much risk you are truly taking and adjust in small steps if your sleep is affected.

EUR Investor’s Note

With the euro above the dollar line, gains from US assets can be trimmed when you convert back, even if the companies do fine. Think about how much you want in foreign markets and whether you balance that with home-currency holdings.

above parity implies a US dollar headwind; below parity implies a tailwind

Risks & Good Habits

- Avoid chasing markets or regions that already had very strong gains lately

- Avoid putting too much into stories that depend on very cheap money returning

- Keep a simple written plan for how you add or reduce risk, then follow it

- Review fees and products once in a while so your money is not silently drained

- Revisit your goals each year so your investments still match your real life plans

One Decision Today

Choose a calm, regular day each month to review your portfolio and stick to it.

Stay steady, keep learning, and let time in the market work for you.